2019

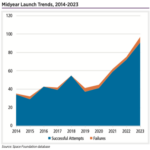

Midyear Launch Trends, 2014-2023

The first half of 2023 saw 97 launches worldwide, setting a record pace despite delays for major rocket programs that pushed the debuts of two major launch vehicles later into the year and notable failures on launch for SpaceX’s Starship in America and Mitsubishi’s H3 in Japan.

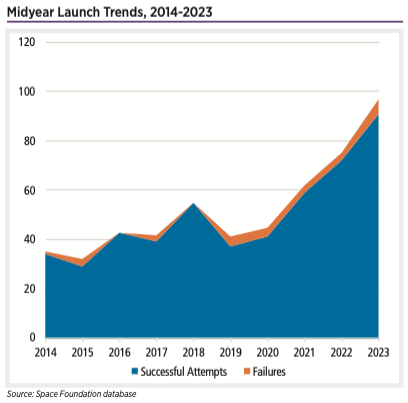

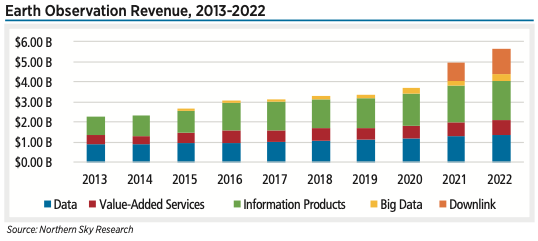

Earth Observation Revenue, 2013-2022

Earth observation satellites circle the globe collecting images and information about the Earth. This information can be valuable for a wide array of applications such as fishing, mining, and weather forecasting. Some companies in this sector sell satellite observations and imagery directly, as individual products or as a more continuous downlink, while others focus on the sale of value-added products and services or big data analyses derived from the satellite data.

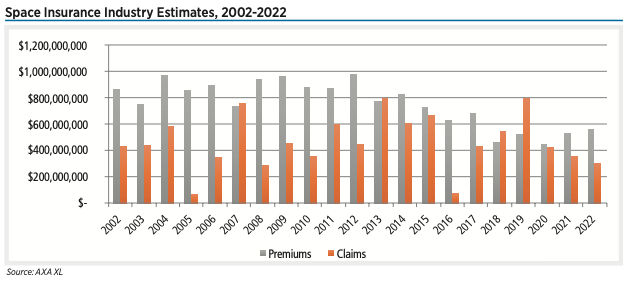

Space Insurance Industry Estimates, 2002-2022

Operating in the space sector involves risks. Space launch is complex and launch failures are possible, even for well-established vehicles. New vehicles typically carry even greater risk. Once spacecraft successfully reach orbit, issues may arise due to factors such as space weather, space debris and a crowded orbital environment. To deal with these risks, many companies in the space sector invest in space insurance. As of 2023, there were about 25 direct space insurance companies worldwide.

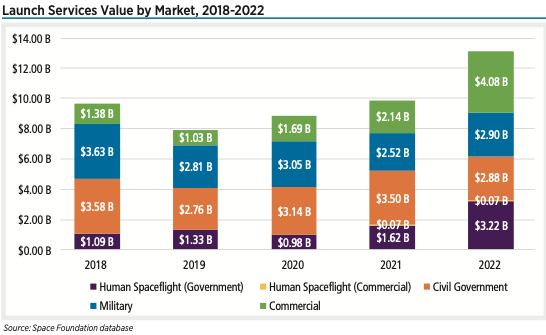

Launch Services Value by Market, 2018-2022

There were 186 launch attempts in 2022, up 28% from 145 attempts in 2021. Of these launches, 179 were successful. Commercial launches, defined as launches carried out for a non-government customer, accounted for 81 of the attempts and 79 of the successes in 2022. This is a significant increase from the 55 commercial launch attempts in 2021.1 The total market value of launches in 2022 was $13.2 billion, based on analysis by Eurospace, the trade association of the European Space Industry.

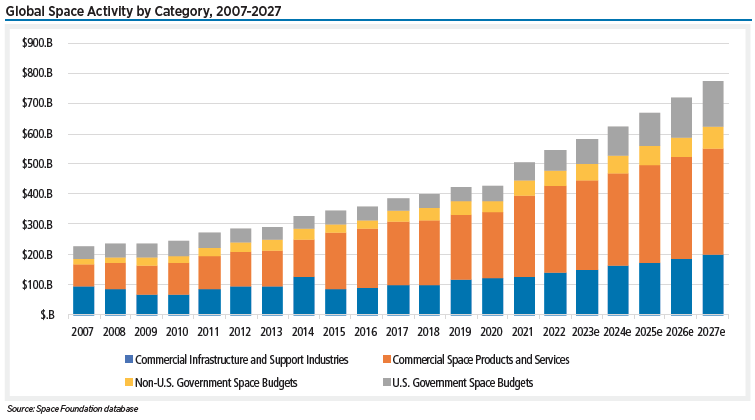

Global Space Activity by Category, 2007-2027

Based on global economic factors, Space Foundation forecasts that growth will slow slightly in 2023 to 6% before picking up for an average five-year growth of 7%. Under these conditions, the space economy would total $772 billion in 2027. This forecast incorporates existing markets in the space economy and does not predict any future disruptive technologies that could have extraordinary growth over the coming years.

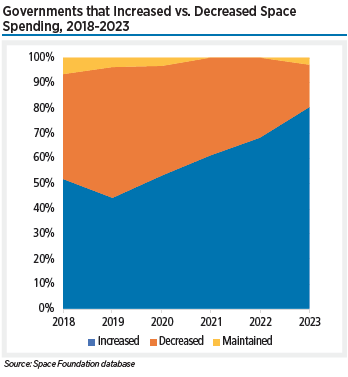

Governments that Increased vs. Decreased Space Spending, 2018-2023

Governments are continuing to grow their space programs at a rapid pace in 2023, preliminary data for 36 nations show. The proportion of nations that increased spending in 2023 reached 81% compared to 68% last year and 52% five years ago.

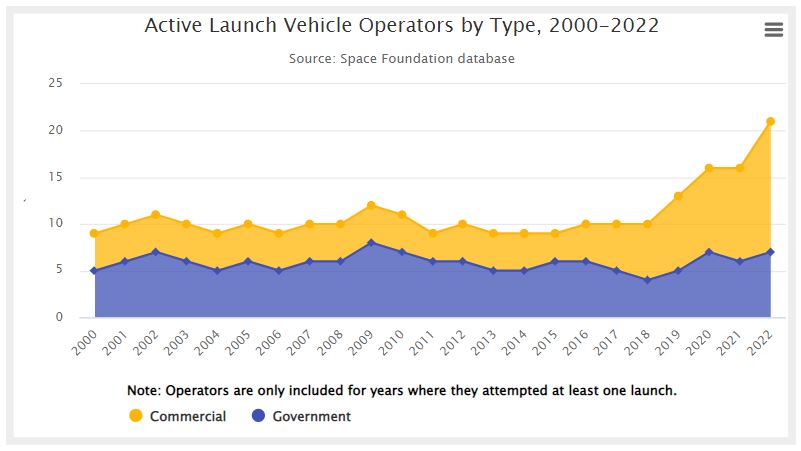

Active Launch Vehicle Operators by Type, 2000-2022

Orbital launch attempts have more than tripled since a lull in activity in the early 2000s bottomed out at 55 attempts in 2004. Part of the rapid growth in the past few years is due to a sharp increase in launch vehicle operators after a long period with an average just shy of 10 distinct operators per year.

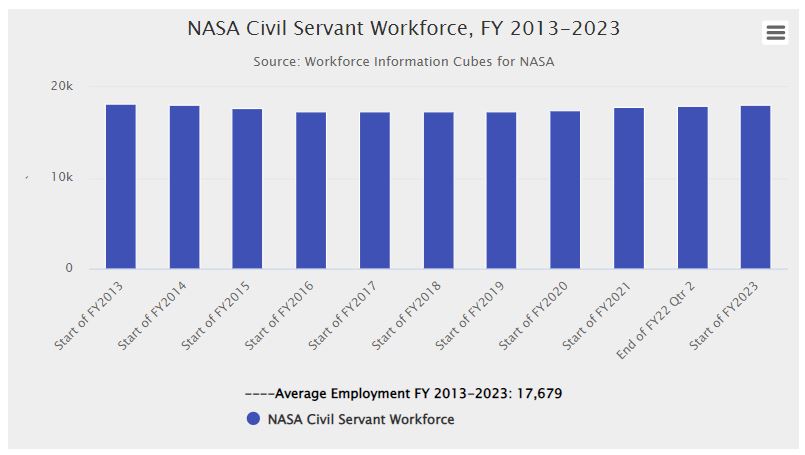

NASA Civil Servant Workforce, FY 2013-2023

In 2022, NASA was named the best place to work in the federal government among large agencies for the 10th year in a row. NASA attributed this “decade of excellence” to the agency’s continuing dedication to supporting and strengthening its workforce.

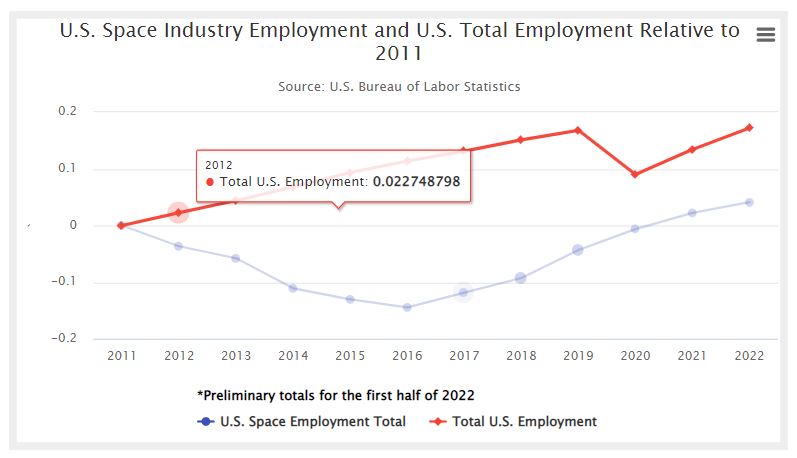

U.S. Space Industry Employment and U.S. Total Employment Relative to 2011

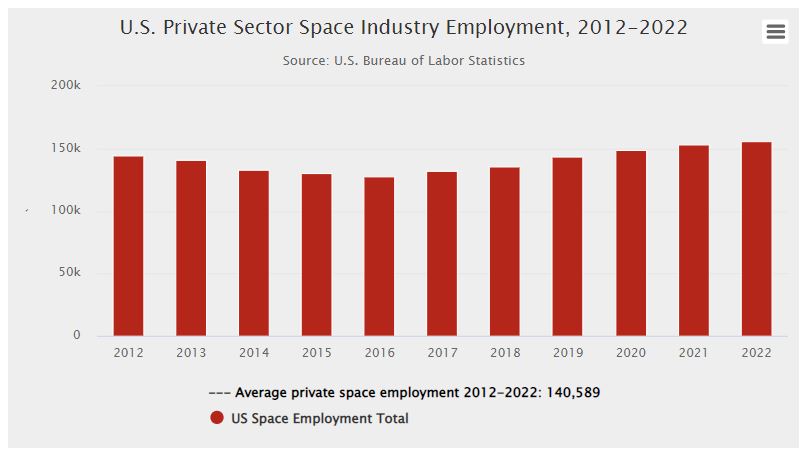

Employment at U.S. private sector space companies grew nearly 2% from 2021 to 2022, reaching 155,973 people in five employment classifications, based on preliminary estimates from the U.S. Bureau of Labor Statistics. This continues a consistent pattern of growth since 2016.

U.S. Private Sector Space Industry Employment, 2012-2022

The private space sector has grown more than 18% over the past five years and proved to be resilient to the negative effects on total U.S. employment associated with the COVID-19 pandemic.